This differs from the standard approach, under which the full amount of each supplier invoice is initially recorded, with any early payment discounts recorded only when payment is eventually made. The journal entry to account for purchase discounts is different between the net method vs the gross method. The net method initially records the purchase at net price (i.e. gross price less the potential discount).

What are some drawbacks to using net method of recording purchase discounts?

Read each section in this chapter, which explains the purpose of the balance sheet, income statement, and the cash flow statement. You should get as much practice working on these statements as you can, since they are the fundamental information on any organization. The following example provides the journal entries to record inventory purchase using gross method and net method under periodic inventory system. Regarding tracking purchase discounts, there are two essential methods – the net method and the gross method.

Gross Method of Accounting for Cash Discounts

- A business that offers cash discounts on credit sales can use the gross method to account for those sale.

- One of the primary differences between the two methods lies in the timing and accuracy of financial reporting.

- Our team of reviewers are established professionals with decades of experience in areas of personal finance and hold many advanced degrees and certifications.

- This method also facilitates more accurate budgeting and resource allocation, as it provides a clear understanding of the company’s income before any deductions are applied.

You can look at past expenses, deductions, and discounts to help avoid financial shortfalls in the future. Once you spot an issue, such as decreasing net revenue, you can dive deeper into the deductions to figure out which can be reduced. Each number represents a key part of a company’s financial health and its progress toward current goals. However, in addition to calculating them differently, gross and net revenue provide different types of information to the company. It would be wrong to record $10,000 as a debit to Marketing Consulting Expenses and to record a credit of $100 in the account Cash Discounts.

Consolidated Balance Sheets: Key Elements and Common Challenges

Because gross revenue shows potential market size, organizations can use this value to guide decisions about expanding operations, entering new markets and investing in new products. For example, a high gross revenue indicates that there is a high demand for your product or service. If you have the ability to compare your gross revenue to competitors, you might be able to determine whether there’s a larger market size than the one you are serving. You can also use net revenue to guide decisions on pricing, customer management, and cost control, directly affecting the bottom line. Imagine that a business, “Gadget Store”, purchases 100 units of a product for $10 each. This means the supplier is offering a 2% discount if the invoice is paid within 10 days; otherwise, the full amount is due in 30 days.

Amount at which sales are recorded

Tools like aging schedules and historical data can help businesses make these estimates more accurately. By proactively managing uncollectible accounts, companies can maintain the integrity of their financial statements and ensure that their reported revenues and receivables are realistic. This practice is particularly important for businesses with a high volume of credit sales, where the risk of uncollectible accounts is more significant.

For example, suppose you sell original artwork to a home store for $500 on terms of 2/10 net 30. If the home store pays for the artwork within 10 days of the sale, enter a $500 credit to accounts receivable, a debit to cash of $490 and a debit to sales discounts of $10. A sales discount is a reduction in the price of a product or service that is offered by the seller, in exchange for early payment law firms and client trust accounts by the buyer. A sales discount may be offered when the seller is short of cash, or if it wants to reduce the recorded amount of its receivables outstanding for other reasons. Cash discount forfeited would be recorded as an income in case cash discount is not availed. Most businesses do not offer early payment discounts, so there is no need to create an allowance for sales discounts.

This method also facilitates more accurate budgeting and resource allocation, as it provides a clear understanding of the company’s income before any deductions are applied. Consequently, businesses can make more informed decisions regarding investments, expansions, and other strategic initiatives. This includes the illustration of the net method vs gross method of recording purchase discounts both under the perpetual inventory system and periodic inventory system. Like the gross method of recording sales discounts, the gross method of recording purchase discounts is very common. Since the net method assumes the discount will be taken, businesses must be diligent in making timely payments to realize the anticipated savings. Tools like QuickBooks or Xero can automate this process, ensuring that discounts are accurately applied and payments are made within the stipulated time frame.

To decide on a method, consider the size and scope of your business, any special needs or challenges it may face, and what stage of growth you are currently in.

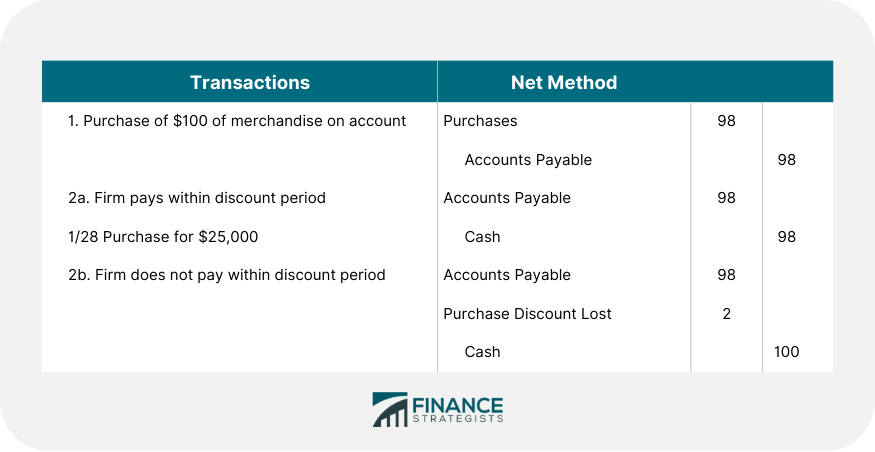

In this method, the discount received is recorded as the reduction in merchandise inventory. Therefore, the amount of discount is recorded on credit to the merchandise inventory account. The net price method is the most theoretically correct way to record supplier invoices, since the effects of discounts are taken into account at once, rather than in a later accounting period. O If goods are sold F.O.B. shipping point, freight prepaid, the seller prepays the trucking company as an accommodation to the purchaser. That is, the seller expects payment for the merchandise and a reimbursement for the freight. In this section, we illustrate the journal entry for the purchase discounts for both net methods vs gross method under the periodic inventory system.

If the buyer does not take advantage of the discount and pays later, no discount is recorded in the accounting records. It’s a shorthand for expressing the discount the buyer receives for paying off purchases within a set period, as well as the ultimate due date. For example “2/10 net 30” states that you receive a 2 percent discount if you pay for your purchase within 10 days, but that in any event the cash is due within 30 days. On an annualized basis, this amounts to 365 days divided by 20 days and multiplied by 2 percent, or 36 percent.

But net revenue is also critical, as it reflects the company’s ability to turn sales into actual earnings, indicating operational efficiency and profitability. According to the net method, the company would initially record the sale at net price. If the invoice is paid within the first ten days, Big Guitar, LLC would be able to record the payoff at the discounted price. Hence, the total accounts payable become a total of $15,000 ($1,470 + $30) the same as the original invoice amount.