A brief reflection, however, should indicate that it would be unusual for a buyer and seller to reach an agreement on an exchange without some idea of the value of the assets or stock. She is a Business Content writer and Management contributor at 12Manage.com, where she contributes a business article weekly. She has over 2 years of experience in writing about accounting, finance, and business.

Non-Cash Item Definition in Banking and Accounting

So the value of the services should be expensed in the period the benefit is received, right? If we receive the benefit, well, we’re going to have an expense. The Apartment Depot exchanged 200,000 shares of 50¢ par value common stock for legal services with a fair market value of $140,000. So if we hadn’t paid him in common stock, we would have had to pay him in cash of $140,000. We receive these legal services, and we’re going to assume that we already used the legal services, right?

The Sale of Stock for Cash

Figure 14.5 shows what the equity section of the balance sheet will reflect after the preferred stock is issued. The structure of a journal entry for the cash sale of stock depends upon the existence and size of any par value. Par value is the legal capital per share, and is printed on the face of the stock certificate. This journal entry will remove both cost and accumulated depreciation of machine. It also record the new land into balance sheet along side with gain on exchange. One prominent challenge involves the subjective nature of assumptions used in valuation techniques.

- This book may not be used in the training of large language models or otherwise be ingested into large language models or generative AI offerings without OpenStax’s permission.

- Textbook content produced by OpenStax is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike License .

- The Apartment Depot exchanged 200,000 shares of 50¢ par value common stock for legal services with a fair market value of $140,000.

- Companies without a trading stock value can also issue new shares to specific investors.

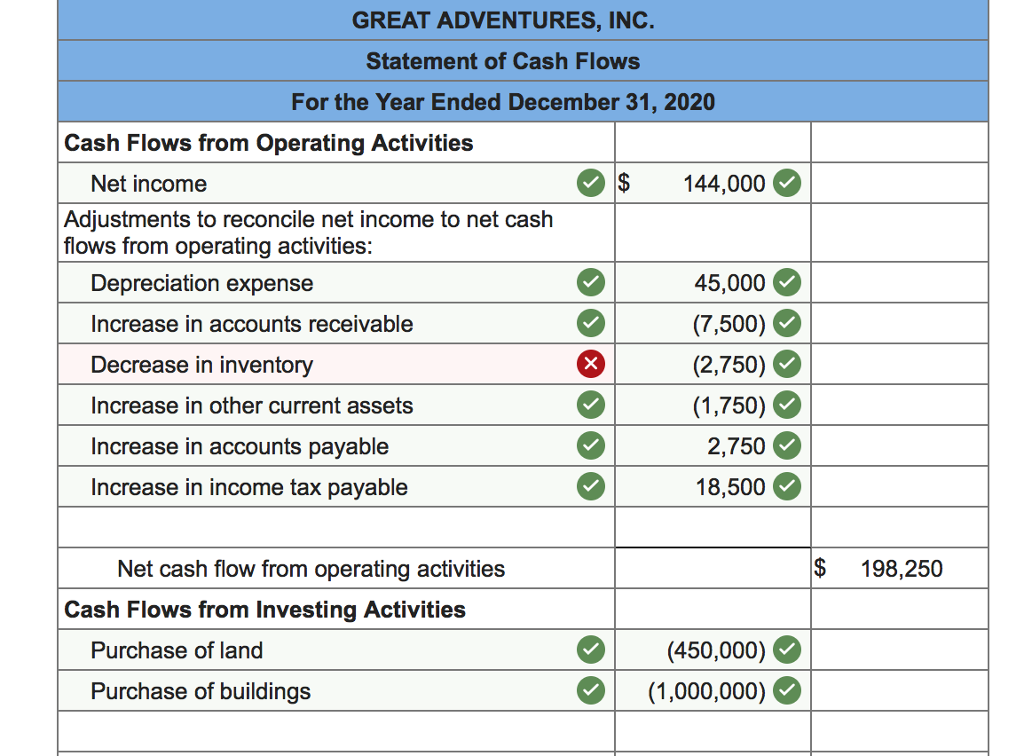

- Depreciation and amortization, being non-cash expenses, are added back to net income in the operating activities section.

Depreciation and Amortization Example

If the shares have a trading value, then the company can use the stock price on the transaction date. When a company issues new shares with no trade value, it has to determine the fair market value of the shares. Non-quoted and quoted companies can issue new stocks with no traded value under special circumstances. Most commonly, private companies issue new shares without a trade value to attract specific investors. A company may also issue new shares through a rights issue or in the form of preferred shares to specific investors. The accounting treatment for the issuance of new shares depends on the market value and the form of consideration received.

Search

Similarly, changes in working capital items, such as accounts receivable and payable, can reflect non-cash movements that impact the company’s short-term financial health. A company may issue common stocks or preferred stocks to raise capital from the market. The sale of new shares in exchange for cash is the most common scenario.

When a company purchases treasury stock, it is reflected on the balance sheet in a contra equity account. As a contra equity account, Treasury Stock has a debit balance, rather than the normal credit balances of other equity accounts. In substance, treasury stock implies that a company owns shares of itself. Treasury shares do not carry the basic common shareholder rights because they are not outstanding. Dividends are not paid on treasury shares, they provide no voting rights, and they do not receive a share of assets upon liquidation of the company. There are two methods possible to account for treasury stock—the cost method, which is discussed here, and the par value method, which is a more advanced accounting topic.

The valuation of carbon credits can be complex, involving market-based pricing and regulatory considerations. Proper accounting for these credits not only ensures compliance with environmental regulations but also enhances the company’s reputation as a socially responsible entity. The tax implications of non-cash transactions are multifaceted and can significantly influence a company’s tax liability and overall financial strategy. Understanding these implications is essential for effective tax planning and compliance. For instance, barter transactions, while not involving cash, are still considered taxable events. The fair market value of the goods or services exchanged must be reported as income, and corresponding deductions can be claimed for the expenses incurred.

Depreciation and amortization are perhaps the two most common examples of expenses that reduce taxable income without impacting cash flow. Companies factor in the deteriorating value of their assets over time in a process known as depreciation for tangibles and amortization for intangibles. The landscape of non-cash transactions how to claim a new child on your taxes is continually evolving, with innovative methods emerging to meet the changing needs of businesses. One such method is the use of cryptocurrency for transactions. Companies are increasingly exploring the use of digital currencies like Bitcoin and Ethereum for various purposes, from paying suppliers to compensating employees.

11 Financial’s website is limited to the dissemination of general information pertaining to its advisory services, together with access to additional investment-related information, publications, and links. Textbook content produced by OpenStax is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike License . This book uses the Creative Commons Attribution-NonCommercial-ShareAlike License and you must attribute OpenStax. These materials were downloaded from PwC’s Viewpoint (viewpoint.pwc.com) under license. The company comes to the agreement to exchange machine with a piece of land which has a market value of $ 900,000. We get this value from the local real estate agency which is considered reliable.